Linear Regression Maths

In this blog I

will be writing about Linear Regression, that is, what is linear regression,

finding best fit regression line, checking goodness of fit etc.

So without any

further due lets get started.

Before we dive into Linear regression lets

understand what is regression and what are its use cases.

What is Regression?

Regression is a statistical method

used in finance, investing, and other disciplines that attempts to determine

the strength and character of the relationship between one dependent variable

(usually denoted by Y) and a series of other variables (known as independent

variables).

Uses of Regression

Well there are plenty of use cases for regression but I will mention 3 major applications.

1. Determining the strength of predictors

2. Forecasting an effect

3. Trend forecasting

Linear vs Logistic

regression

What is Linear

Regression?

Linear regression analysis is the most widely used of all statistical techniques: it is the study of linear, additive relationships between variables. Let Y denote the “dependent” variable whose values you wish to predict, and let X1, …,Xk denote the “independent” variables from which you wish to predict it, with the value of variable Xi in period t (or in row t of the data set) denoted by Xit. Then the equation for computing the predicted value of Yt is:

Where Linear Regression is used?

1. Estimating Trends and Sales Estimates

2. Analyzing the impact of Price Changes

3. Assessment of risk in financial services and insurance

domain

In this blog I’m going to focus

only on variable selection for Linear Regression, explaining three approaches

which can be used:

·

Best Subset Selection

·

Forward Stepwise Selection

·

Backward Stepwise Selection

This approach tries all the

possible 2^p combinations of inputs with the following idea. It starts from the

null model, containing only the intercept:

Next, it trains other 6 models with

all the possible combinations of couples of variables and then pick, again the

one with lowest RSS or highest R²:

Then, we are left with 4 selected

model with, respectively, 1, 2, 3 and 4 variables. The final step is picking

the best one using metrics as Cross-Validation or

adjusted error metric (adjusted R², AIC, BIC…), in order to take into

consideration the bias-variance

trade off.

2. Forward Stepwise Selection

With forward selection, we follow a

similar procedure as before, with one important difference: we keep trace of

the selected model at each step and only add variables, one at the time, to

that selected model, rather that estimate one new model every time.

So we start again from the null

model and repeat the first step above, that is training 4 models with 1

variable each and pick the best one:

3. Backward Stepwise Selection

The idea of this approach is

similar to the Forward Selection, but in reverse order. Indeed, rather than

starting from the null model, we start from the full model and remove one

variable at the time, keeping trace of the previously selected model.

So, moving from the full model:

The main difference between Forward

and Backward approach is that the former can deal with task where p>n (it

simply adds a stopping rule when p=n), while the latter cannot, since the full

model implies p>n.

Now to let us know about internal theory to built our

Linear regression Model

Line of Best Fit

A Line of best

fit is a straight line that represents the best approximation of

a scatter plot of data points. It is used to study the nature of the

relationship between those points.

The equation to find the best

fitting line is:

Y` = bX + A

where, Y` denotes the predicted

value , b denotes the slope of the line ,

X denotes the independent variable,

A is the Y intercept

Usually, the apparent predicted

line of best fit may not be perfectly correct, meaning it will have “prediction

errors” or “residual errors”.

Prediction or Residual error is

nothing but the difference between the actual value and the predicted value for

any data point. In general, when we use Y` = bX +A to predict the actual

response Y`, we make a prediction

error (or residual error) of size:

E = Y — Y`

where, E denotes the prediction

error or residual error

Y` denotes the predicted value

Y denotes the actual value

A line that fits the data “ best” will be one for which the prediction errors (one for each data point) are as small as possible.

The below diagram depicts the

simple representation with all the above discussed values:

What is R-Square?

1. R-squared value is a statistical measure of how close

the data are to the fitted regression line

2. It is also known as coefficient

of determination, or the coefficient

of multiple determination.

Formula

The R-squared formula is calculated

by dividing the sum of the first errors by the sum of the second errors and

subtracting the derivation from 1. Here’s what the r-squared equation looks

like.

R-squared = 1 —

(First Sum of Errors / Second Sum of Errors)

First, you use the line of best fit

equation to predict y values on the chart based on the corresponding x values.

Once the line of best fit is in place, analysts can create an error squared

equation to keep the errors within a relevant range. Once you have a list of

errors, you can add them up and run them through the R-squared formula.

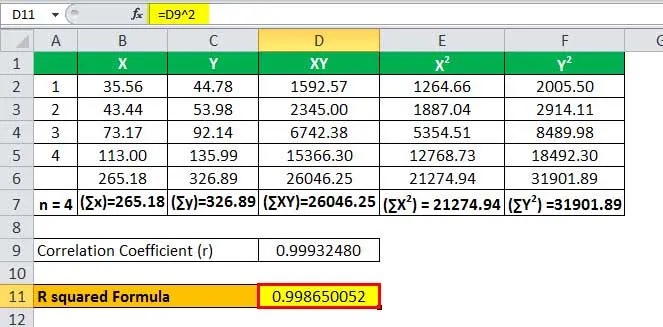

Example

Consider the following two

variables x and y, you are required to calculate the R Squared in Regression.

Using the above-mentioned formula,

we need to first calculate

the correlation coefficient.

Let’s now input the values in the

formula to arrive at the figure.

r = 17,501.06 / 17,512.88

The Correlation Coefficient will be-

So, the calculation will be as

follows,

R Squared Formula in Regression

I tried to provide all the important information on

getting started with Linear Regression and its implementation. I hope you will find something useful here. Thank

you for reading till the end.

Comments

Post a Comment